|

| Police at SVB HQ in Santa Clara (Mercury News) |

However, the latter possibility affected the stock market, whose major indices were down between 1 and 2%. [bold added]

SVB Financial bought tens of billions of dollars of seemingly safe assets, primarily longer-term U.S. Treasurys and government-backed mortgage securities...These securities are at virtually no risk of defaulting. But they pay fixed interest rates for many years. That isn’t necessarily a problem, unless the bank suddenly needs to sell the securities. Because market interest rates have moved so much higher, those securities are suddenly worth less on the open market than they are valued at on the bank’s books. As a result, they could only be sold at a loss.The failure of SVB is symbolically meaningful because it puts an exclamation mark on the decline of the tech industry in California. SVB's customers are concentrated in tech, and the steep rise in interest rates over the past year has made risky investments in those customers much less attractive.

SVB’s unrealized losses on its securities portfolio at the end of 2022—or the gap between the cost of the investments and their fair value—jumped to more than $17 billion.

At the same time, SVB’s deposit inflows turned to outflows as its clients burned cash and stopped getting new funds from public offerings or fundraisings. Attracting new deposits also became far more expensive, with the rates demanded by savers increasing along with the Fed’s hikes. Deposits fell from nearly $200 billion at the end of March 2022 to $173 billion at year-end 2022.

In California financial stress has been exacerbated by high taxes and regulations, which have caused high-profile companies like HP, Oracle, and Tesla to move out of State. It is easy to imagine that the run on California's premier tech bank is related to the exodus of businesses out of the State.

|

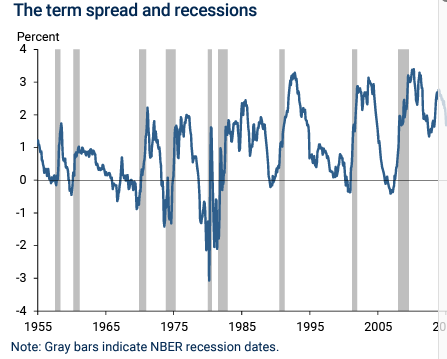

| A negative number indicates the 1-year Treasury rate is greater than the 10-year. (SF Federal Reserve) |

"If you lock your money up for a longer period of time, you almost always get a higher interest rate..."However, today, things are backwards - 10-year interest rates are far below short-term rates. This is known as an 'inverted yield curve.' In the past 50 years, we have seen seven inverted interest rate curves. Each one was followed by a recession."Silicon Valley Bank bet that normal would continue. That bet proved disastrous when it kept having to refinance deposits and other short-term borrowings as rates climbed rapidly higher. Major banks are required to "stress test" for just such an eventuality; let's hope they didn't cut corners.

No comments:

Post a Comment